Summary

- Amazon has found itself in a tough spot, struggling to maintain the momentum in FCF

- Long-term survival of their Retail and AWS businesses on proving short-term as well as long-term profitability

Thesis

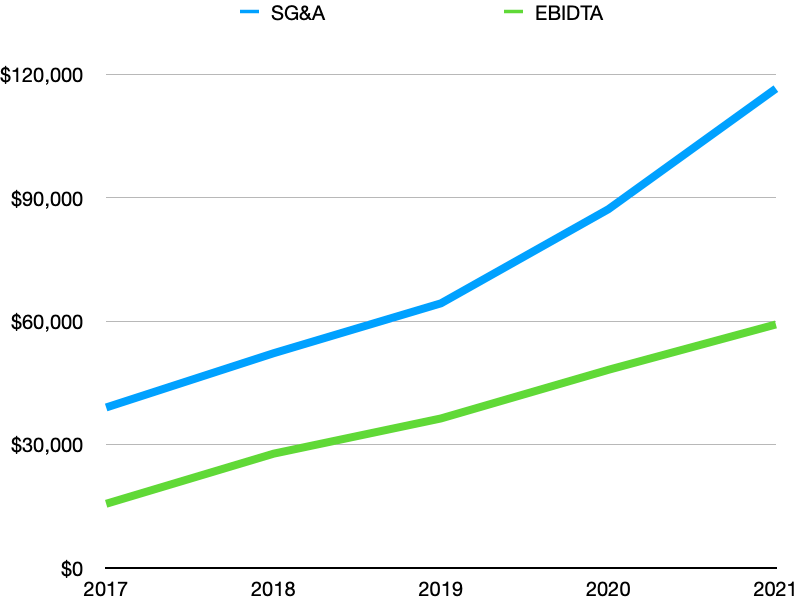

Amazon had strong growth during the pandemic, with more people spending time online shopping. This may have resulted in the leadership at these companies becoming overly optimistic on future growth resulting in rapid headcount growth. <At AMZN, the SG&A expenses are much higher than the EBIDTA> and this is not sustainable. In this high interest rate environment, the market is no longer as forgiving.

| Year | EBIDTA | SG&A |

| 2019 | $36,330 | $64,313 |

| 2020 | $48,150 | $87,193 |

| 2021 | $59,175 | $116,485 |

Short term challenges

For Amazon, the major headwinds could be categorized as follows

- Amazon enjoyed stock valuation multiples above high double digits for a the past 4 years, thanks to the rapidly growing AWS business, strong competition in the form of compelling cloud offerings from Microsoft and Google is starting to make a meaningful dent

- No meaningful revenue sources outside of AWS have materialized, meaning that Amazon relies heavily on AWS revenue. (Source:1. <earnings report> 2. https://appeconomyinsights.substack.com/p/amazon-day-1)

Long term Prospects

Amazon is taking steps in the right direction to trim costs and become cost efficient. AWS continues to hold a large market share and is continuing to pull in profits <earnings report>.

I believe trimming down the longer term/higher risk bets such as their hardware division is the right thing to do. Hardware projects have a high upfront over head and their current model of selling hardware at cost or subsidized in some cases is detrimental to their bottom line. A leaner strategy would be to double down their existing licensing program(https://developer.amazon.com/en-US/alexa/devices/connected-devices/business-resources/works-with-alexa ) for Alexa to save cost while delivering the same value to their customer.

Amazon still holds a dominant position on the E-Commerce space (https://www.pymnts.com/news/retail/2022/amazons-share-of-us-ecommerce-sales-hits-all-time-high-of-56-7-in-2021/), once they are able to develop a sustainable model to monetize this large user base, success is guaranteed!

To summarize, based on the dominant position in the Cloud arena with AWS and dominance in the e-commerce space, I believe the stock has a lot of room to move up in the long term, making the current market slump a great opportunity to get in.

Leave a comment